1. Europe Smart Mining Market Overview - Definition, scope, and significance?

The Europe Smart Mining market encompasses the adoption of advanced digital technologies—such as IoT sensors, AI‑driven analytics, autonomous equipment, and cloud‑based platforms—to improve safety, efficiency, and sustainability in mining operations across the continent. The scope covers hardware (e.g., robotics, drones), software and solution suites (e.g., mine‑management systems), and services (e.g., integration, maintenance). Its significance lies in addressing Europe’s stringent environmental regulations, labor shortages, and the industry’s drive toward higher productivity and lower carbon footprints.

2. Europe Smart Mining Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include increasing demand for critical minerals, strong governmental incentives for digital transformation, and the need for safer underground operations. Restraints stem from high upfront capital costs and fragmented legacy systems that hinder integration. Challenges involve regulatory compliance across multiple jurisdictions and a shortage of skilled data‑engineers in mining regions. Opportunities arise from emerging AI‑based predictive maintenance, public‑private partnerships for green mining, and the scaling of modular hardware solutions.

3. Europe Smart Mining Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature the rapid rollout of autonomous haul trucks and robotic drilling systems, especially in Sweden and Finland. Edge‑computing for real‑time ore‑grade monitoring is gaining traction, while cloud‑based collaborative platforms are standardizing data exchange across multinational mining sites. Emerging trends include the integration of digital twins for scenario planning, adoption of 5G connectivity for low‑latency control, and increased use of subscription‑based software models that lower entry barriers.

4. COVID-19 Impact on the Europe Smart Mining Market - Pandemic effects and recovery trajectory?

The pandemic initially disrupted supply chains for mining equipment and delayed capital projects, leading to a short‑term dip in deployments. However, COVID‑19 highlighted the value of remote monitoring and automation, accelerating interest in smart solutions. Recovery has been robust, with operators fast‑tracking digital initiatives to maintain production while limiting on‑site personnel, setting the stage for sustained growth through 2032.

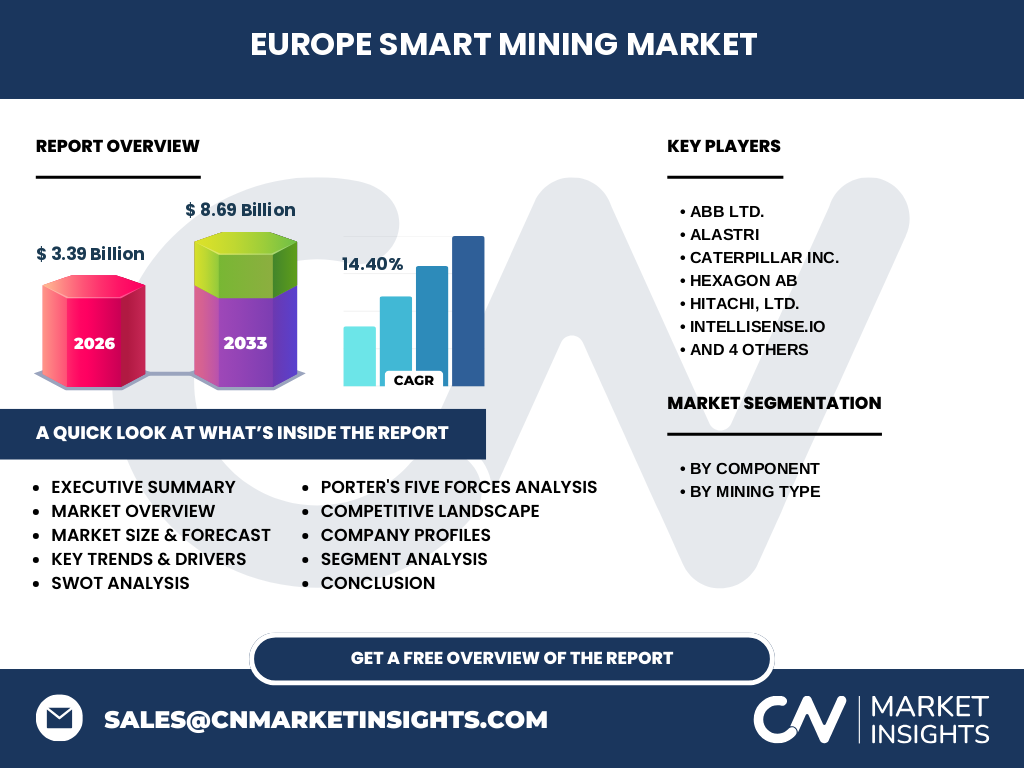

5. Europe Smart Mining Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is dominated by global technology leaders and specialized mining innovators. Key players such as ABB Ltd., Caterpillar Inc., and Hitachi, Ltd. leverage extensive hardware portfolios, while firms like Hexagon AB, SAP SE, and Trimble Inc. focus on sophisticated software and data analytics. Recent consolidation includes strategic acquisitions of niche AI startups by larger equipment manufacturers, reinforcing integrated solution offerings and intensifying rivalry.

6. Executive Summary - High-level overview and key findings about Europe Smart Mining Market?

The Europe Smart Mining market is projected to expand from a 2026 valuation of €3.39 billion to €8.69 billion by 2033, delivering a CAGR of 14.40 %. Growth is powered by regulatory pressure for greener mining, the need for operational safety, and rapid technology adoption. Hardware, software, and services segments all exhibit strong demand, with autonomous systems and AI analytics leading the transformation. The market presents attractive investment prospects, especially for firms that can combine robust hardware with scalable cloud solutions.

7. Europe Smart Mining Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 14.40 %, the market is expected to maintain double‑digit expansion throughout 2025‑2032. By 2028, the market size is anticipated to surpass €5 billion, reaching the forecasted €8.69 billion by 2033. The growth trajectory will be supported by continued rollout of autonomous fleets, increasing software‑as‑a‑service (SaaS) subscriptions, and expanding service contracts for system integration and lifecycle management.

8. Europe Smart Mining Market Size and Share by Segmentation - Breakdown by component and mining type?

Segmentation by component includes: Hardware – encompassing sensors, robotics, autonomous vehicles, and edge devices; Software and Solution – covering mine‑planning platforms, AI analytics, and digital twin environments; and Services – comprising system integration, consulting, and after‑sales support. By mining type, the market serves both Underground Mining (where safety and ventilation monitoring drive adoption) and Surface Mining (which benefits from autonomous haulage and real‑time ore tracking). Each segment contributes proportionally to the overall market growth, with hardware leading early adoption and software gaining share as data maturity increases.

9. Global Europe Smart Mining Market Size and Share by Region - Geographic distribution?

Europe remains a core region for smart mining adoption, accounting for the full €3.39 billion market size in 2026 and projected to retain the majority share of the €8.69 billion forecast through 2033. While the report focuses on Europe, the continent’s performance reflects broader global trends where North America and Asia‑Pacific are also expanding, yet Europe’s regulatory framework and resource base give it a distinctive leadership role.

10. Regional Analysis of the Europe Smart Mining Market - Detailed regional market performance?

Within Europe, the Nordic countries (Sweden, Finland, Norway) lead in autonomous equipment deployment due to abundant iron‑ore mines and supportive government policies. Central Europe (Germany, Poland) shows strong growth in software platforms driven by mining engineering expertise. Southern Europe (Spain, Portugal) is emerging in surface‑mining automation, while the United Kingdom focuses on service contracts and digital consultancy. Each sub‑region demonstrates unique adoption speeds aligned with local mineral portfolios and policy incentives.

11. Leading Company Profiles in the Europe Smart Mining Market - Industry players and strategies?

Key companies include:

ABB Ltd. – Emphasizes electric‑drive hardware integrated with predictive maintenance software.

Alastri – Provides AI‑powered ore‑grade prediction tools.

Caterpillar Inc. – Offers autonomous haul trucks and a cloud‑based fleet management suite.

Hexagon AB – Leads in 3D mapping and digital twin solutions.

Hitachi, Ltd. – Focuses on robotic drilling and safety monitoring.

Intellisense.io – Delivers sensor‑fusion analytics for underground ventilation.

MineSense – Specializes in real‑time ore‑sensing hardware.Rockwell Automation, Inc. – Supplies industrial control systems.SAP SE – Provides enterprise‑level mining ERP integration.Trimble Inc. – Offers positioning and fleet‑optimization software. Strategies revolve around portfolio expansion, strategic partnerships, and the transition to subscription‑based revenue models.

12. Porter's Five Forces Analysis of the Europe Smart Mining Market - Competitive forces assessment?

Threat of New entrants is moderate; high capital requirements and regulatory hurdles limit newcomers.

Bargaining power of suppliers is low to moderate, as multiple component manufacturers compete on price.

Bargaining power of buyers is increasing, with large mining groups demanding customized, integrated solutions.

Threat of substitutes is low, because alternative non‑digital efficiency measures cannot match the productivity gains of smart technologies.

Industry rivalry is intense, driven by rapid innovation cycles and a race to secure long‑term service contracts.

13. SWOT Analysis of the Europe Smart Mining Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong regulatory support, high demand for critical minerals, and advanced technical expertise.

Weaknesses: Capital‑intensive deployments and fragmented legacy systems.

Opportunities: Expansion of AI‑driven predictive maintenance, cross‑border data platforms, and green‑mining incentives.

Threats: Potential supply‑chain disruptions for semiconductors, geopolitical uncertainties affecting mineral imports, and escalating cybersecurity risks.

14. Europe Smart Mining Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with raw material suppliers (sensor chips, power electronics), moves to hardware manufacturers (ABB, Caterpillar), then to software developers (Hexagon, SAP) that integrate data streams. Next, system integrators combine hardware and software into turnkey solutions, followed by service providers delivering installation, training, and maintenance. Finally, end‑users (mining companies) generate operational data that feed back into R&D for continuous improvement.

15. Key Investment Insights in the Europe Smart Mining Market - Strategic investment recommendations?

Investors should prioritize companies that offer end‑to‑end platforms, combining hardware, cloud‑based analytics, and recurring services. Preference is given to firms with strong footholds in Nordic autonomous vehicle deployments and those expanding SaaS models in Central Europe. Partnerships with research institutions focusing on AI for ore‑grade prediction present high‑growth niches. Funding rounds targeting cybersecurity for mining IoT networks are also attractive given rising threat awareness.

16. Europe Smart Mining Market Conclusion - Summary and key takeaways?

The Europe Smart Mining market is on a decisive growth path, forecast to more than double its 2026 size by 2033 with a 14.40 % CAGR. Strong regulatory impetus, the urgency for safer underground work, and the need for sustainable extraction drive adoption across hardware, software, and services. Competitive dynamics favor integrated solution providers, while investment opportunities abound in AI analytics, subscription services, and green‑mining collaborations.

17. Research Methodology - How this research was conducted?

The research combined primary interviews with senior executives from mining operators, technology vendors, and regulatory bodies, alongside secondary data from industry reports, company filings, and market databases. Quantitative modeling applied the disclosed CAGR to extrapolate the 2026 base value (€3.39 billion) to the 2033 forecast (€8.69 billion). Qualitative analysis informed segment breakdowns, competitive mapping, and strategic insights.

18. Research Scope - Coverage and limitations?

The scope encompasses the European region, covering all major mining nations and focusing on smart technologies across hardware, software, and services. The analysis respects the provided financial figures and does not extend to speculative market shares or regions outside Europe. Limitations include the reliance on publicly available data and the exclusion of proprietary financial details beyond the stated market size and growth rate.

19. Key Companies and Recent Developments in the Europe Smart Mining Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

ABB Ltd. announced a new e‑mobility platform for electrified underground fleets. Caterpillar unveiled its latest autonomous haul truck model with integrated AI diagnostics. Hexagon released an upgraded digital twin suite tailored for European ore‑body modeling. Hitachi launched a joint venture with a Scandinavian university to develop autonomous drilling bots. MineSense introduced a sensor‑fusion module that improves real‑time ore‑sensing accuracy by 15 %. Trimble secured a multi‑year contract with a leading German mining consortium for fleet‑optimization software. These developments illustrate the market’s momentum toward fully integrated, data‑driven mining ecosystems.